Photograph by MBN

At a certain point, you have to presume that tossing facts toward the Tea Party is akin to spitting into a hurricane. Stats slide past them, slipping on their protective sheen of “patriotism” and “liberty” and “Reagan.” You can use fact and figure with the folk, but if it doesn’t come draped in star and stripe, and if it’s not buggering on about Agenda 21 and Mexican floods, it’ll likely not gain any traction.

So it goes. But even if you can’t win, even if you can’t crack that epistemic bubble, there’s no shame in continuing the fight, in continuing to sludge numbers and reality at the nationalists clamoring for default and coup d’état. The latest fantasy, as we’ve seen, involves the stake that American default wouldn’t really be all that bad. Just a few bumps on the Dow. Just a few lumps for those on the government dole. Just a few days in which the international financial structure suddenly acknowledges that the insolence and insanity of a few can dominate the salience of the many.

Much of such financial idiocy stems from the belief that, under President Obama, the US has piled public debt at a rate never known. That the debt is “exploding.” (Volcanic imagery is apparently a must when describing such growth.) As such, as this debt grows at ever-expanding pace, we find the logic in attempting to force the US to reach, and break, the debt ceiling. If we’re held below such self-imposed limit, the logic goes, we’ll manage to cut the spending far quicker than any measured legislative discourse can provide. Doesn’t matter if almost every noted economist predicts that we’ll batter the fiscal confidence built so fragilely. Doesn’t matter if financial markets will reel, without any form of precedent to provide any confidence. Those are just predictions, after all.

But then, those predictions, as any worth listening to, are based on facts. And while the facts and figures burgeoning the debt ceiling have been well-trod over the past few weeks, one reality’s been overlooked. While Obama has, indeed, seen more debt pile under his tenure than anyone prior in real terms, the actual rate of growth of the US debt has been, well, quite measured. It’s been on the higher end, sure – but in terms of growth over four-year periods, the swell we’ve seen since 2009 has not been one of the largest stretches the country’s ever known. Hell, it’s barely been in the top 10.

If we’re being generous, we can say that the US debt, currently at $16.7 trillion, has grown 57.6 percent in the four years under Obama. (It’s been a bit more than four years, but, for the sake of argument, let’s pin that percentage to a four-year stretch.) That’s plenty, to be sure. But here’s a graph of rolling four-year growth rates since 1963, per data from the Treasury Department.

US Debt Growth Rate Since 1963, Four-Year Periods

In 1971, for instance, the US posted a 22.04-percent growth over the previous four years, meaning that US debt growth grew 22.04 percent from 1967-1971. Not a bad clip. Lower than what we see today, at least. But it’s nowhere near the 86.10 percent we saw in 1986 – smack in the middle of the Reagan years. Indeed, in ’83, ’84, ’85, ’86, ’87, ’88 – all those four-year averages in which Reagan was the sole presence in the White House – we saw a higher rate of debt growth than anything we’ve seen under the White House’s current tenant. Under Obama, the debt’s grown slightly more than 50 percent. Under Reagan’s first four years, the debt nearly doubled.

Still, though – you can see a bump under Obama. His debt management looks far more worrisome than, say, Clinton or LBJ. But stretch it out a bit more. Take a look at the kind of rates we’ve incurred over the last century, and see if the rhetoric on explosion and eruption still holds:

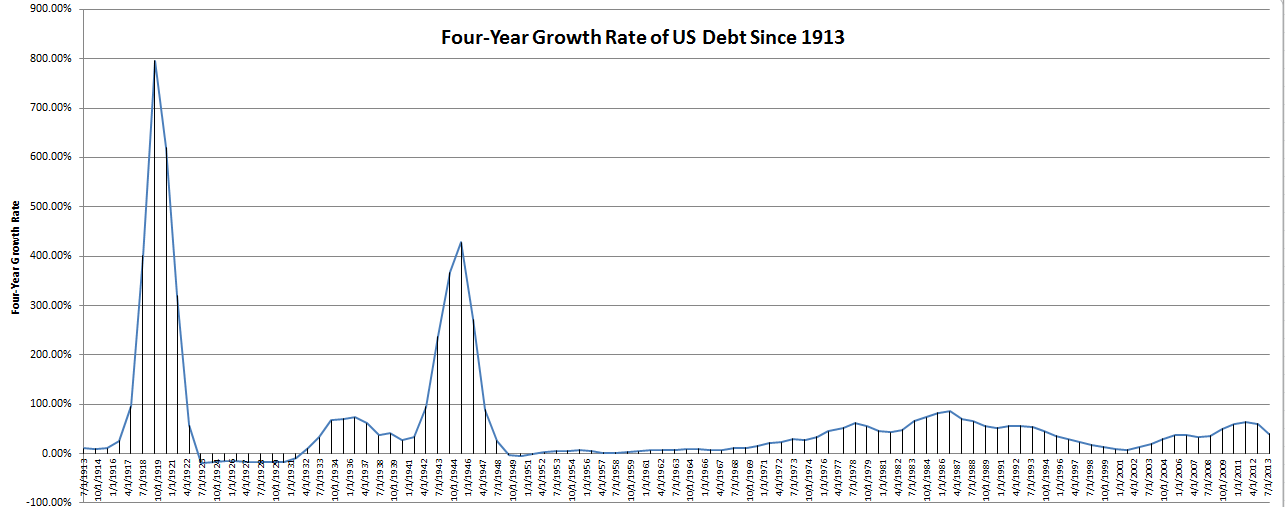

US Debt Growth Rate Since 1913, Four-Year Periods

Not so much. Obama and Reagan both barely manage blips in the graph’s tail, replaced by a pair of war-period spikes. FDR’s New Deal period also registers an observable uptick, but falls off before WWII sets in. It’s funny, actually – the only period that many on the right seem to brook to seeing a rapid debt growth is often WWII. But check the First World War. All told, the debt from 1915-1919 grew by a staggering796 percent. Mobilization, industrial output, transportation necessity – all of this combined to jump America’s debt growth rate to far and away its highest point in the last century. All for a war in which America fought for a mere 20 months.

The 19th century also saw a handful of periods in which the debt grew at an overwhelming clip. However, a graph wouldn’t help much – with the 2,859-percent growth in US debt from 1861-1865, and with a remarkable 30,832-percent growth from 1835-1839, all other periods are flat-lined. Nothing can compare. Not even Obama.

Again, this isn’t to say that the $16.7 trillion currently accrued isn’t an issue. It is. It’s worrisome, and should be rectified sooner rather than later. But the rhetoric? All that screech around debtors’ prisons and Chinese overlords? That needs to stop. That needs to end, because the debt growth we’ve seen over the past four years has not, contra Tea Party types, exploded in unforeseen amounts. It hasn’t run off the rails. And while it’s larger than ever before in empirical terms, the actual growth rate, within the schema of American history, barely registers.

But then, this is all trying to convince those who carry calls of both patriotism and Confederacy. Cognitive dissonance can run deeper than any debt analysis ever will, unfortunately.